Proposal automation explained: streamline insurance sales

TL;DR:

- Proposal automation redefines the entire insurance workflow, connecting intake, rating, document generation, and delivery into a seamless, error-reducing system. It enables agencies to significantly cut quote times, enhance client engagement, and build scalable, exception-proof processes. Successful implementation requires comprehensive coordination across all stages, not just faster document creation.

Most insurance agents assume proposal automation is simply a faster way to print quotes. That assumption costs agencies real money, real time, and real clients. True proposal automation does not just speed up a document. It restructures the entire path from the moment a prospect fills out a form to the moment they sign and bind coverage. This guide breaks down exactly what proposal automation means for insurance agencies, how each stage works, what traps to avoid, and how to apply it for measurable results in your book of business.

Table of Contents

- What is proposal automation?

- How insurance proposal automation works step-by-step

- How automation enhances client engagement and follow-up

- Common pitfalls and advanced considerations in proposal automation

- What most insurance agencies miss about proposal automation

- Next steps: automate your proposals and sales processes

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| End-to-end automation | Proposal automation connects intake, pricing, and digital delivery into one seamless workflow. |

| Improved client engagement | Digital delivery and analytics empower smarter, more timely follow-up with prospects. |

| Insurance-specific needs | Automation must account for exceptions, custom documents, and validation to prevent workflow breakdowns. |

| Templates and rules | A strong rule and template design is key to reliable, flexible automation. |

What is proposal automation?

Proposal automation, in the insurance context, is an end-to-end pipeline that connects intake, rating, document generation, and delivery into a single coordinated workflow. It is not one tool. It is a system of connected stages, each one feeding the next with minimal manual effort.

Think of it this way. Without automation, an agent collects data on paper or by phone, manually enters it into a rating system, copies the output into a Word document, formats it, attaches it to an email, and waits. Every hand-off is a chance for an error, a delay, or a dropped ball. Automation eliminates those hand-offs.

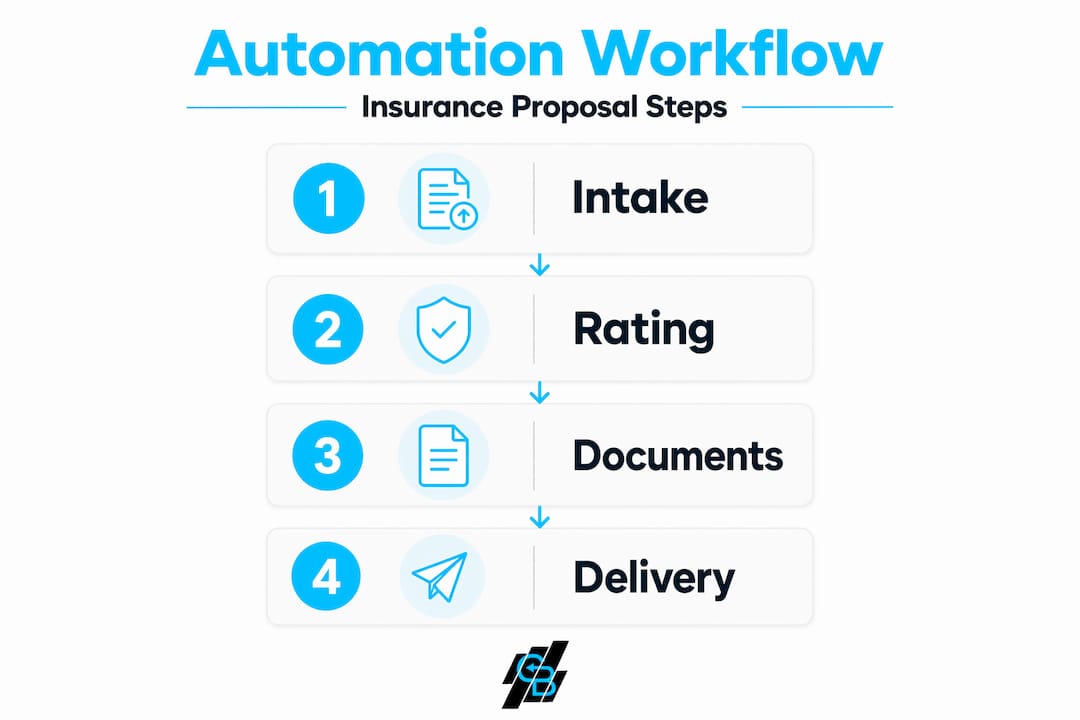

The four core stages of proposal automation

Here is how the full pipeline actually flows in a modern insurance agency setup:

- Intake — Client data collection through digital forms, CRM imports, or AI-assisted intake tools

- Rating and pricing — Carrier APIs or internal rating engines compute the quote in real time

- Document generation — Configured templates produce a client-ready proposal with the right coverage details, branding, and language

- Delivery — The proposal is sent digitally with tracking, e-signature capability, and follow-up triggers

When you optimize your lead funnel properly, each stage feeds automatically into the next without a human having to manually move the process forward.

Manual vs. automated proposal process

| Step | Manual process | Automated process |

|---|---|---|

| Data collection | Phone call, paper form, manual entry | Digital intake form, CRM auto-populate |

| Quote computation | Agent looks up rates by hand | Carrier API returns rate in seconds |

| Document creation | Copy-paste into Word/PDF template | Auto-generated from configured template |

| Delivery | Email attachment, follow up by memory | Digital delivery with tracking and e-signature |

| Error rate | High, especially on repeated tasks | Low, enforced by validation rules |

| Time to quote | 1 to 4+ hours | Under 10 minutes |

The benefits of insurance marketing automation are clearest when you see this comparison side by side. Time savings, fewer errors, consistent branding, and instant digital delivery are not minor perks. They are competitive advantages.

Key benefits at a glance:

- Reduces time-to-quote from hours to minutes

- Eliminates manual data re-entry and transcription errors

- Enforces consistent proposal branding and language

- Triggers digital delivery with real-time engagement tracking

- Frees agents to focus on relationship-building rather than document production

How insurance proposal automation works step-by-step

Understanding the stages is one thing. Seeing how they connect in practice is what makes the difference. Here is a numbered breakdown of the workflow with real-world insurance examples at each step.

Step-by-step automation workflow

-

Intake and data validation — A prospect submits a digital intake form. The system validates required fields before the data even enters the pipeline. Missing a driver’s license number? The form stops the submission and prompts for it. This prevents downstream errors before they happen.

-

CRM enrichment — The validated data is pushed into the CRM, where business rules check for existing records, assign lead scores, and tag the prospect with relevant product lines. An agency specializing in commercial auto can automatically route a prospect who indicates fleet vehicles to a dedicated commercial workflow.

-

Rating engine call — The system sends the cleaned data to carrier APIs or an integrated rating engine. Results come back in seconds for standard risks. For more complex risks, the system flags the record for human review rather than stalling the entire queue.

-

Template-driven document generation — This is where CPQ (Configure, Price, Quote) and document generation tools create client-ready PDFs or Word documents from pre-configured templates and transaction data. Dynamic content rules mean that a flood endorsement, for example, automatically appears in a proposal only when the property is in a FEMA flood zone. Agents do not have to remember to include it.

-

Compliance and brand review rules — Before delivery, automated rules check that required disclosures are present, that the right state-specific language is included, and that the proposal matches brand standards. No more proposals going out without a disclaimer because someone forgot to check.

-

Digital delivery and engagement triggers — The finalized proposal is sent via a tracked link. When the client opens it, the CRM logs the timestamp. If they spend significant time on the premium breakdown section, that behavior triggers a follow-up SMS or email from the agent with a message specifically addressing pricing questions.

Pro Tip: Pre-define templates and content blocks for your 10 most common policy scenarios before you build anything else. This single investment accelerates implementation and cuts error rates dramatically because your automation rules are built around real, tested language rather than generic placeholders.

Automation phase breakdown

| Phase | Manual bottleneck | Automation benefit |

|---|---|---|

| Intake | Incomplete or inconsistent data | Validation rules enforce clean data at the source |

| Rating | Manual carrier lookups | API calls return rates in real time |

| Document generation | Copy-paste errors, formatting issues | Template rules produce consistent, accurate output |

| Compliance check | Agent memory, manual review | Rule-based audit before any proposal leaves the system |

| Delivery | Manual email, no tracking | Digital delivery with open/view/signature tracking |

Well-designed insurance sales automation workflows connect every one of these phases. The result is a process that an agent can initiate in minutes and monitor in real time, rather than babysit across an entire afternoon. The most advanced platforms also incorporate AI marketing tools for agents that can personalize proposal content based on prior interactions, browsing history, or stated coverage priorities.

How automation enhances client engagement and follow-up

Here is something most agents do not think about when they start looking at proposal automation: the proposal is not the end of the process. It is the beginning of the closing conversation. Automation tools transform that conversation by giving agents real data about client behavior.

When a proposal is delivered digitally, the system can track exactly which sections a prospect reads, how long they spend on each one, and whether they forwarded it to someone else. That data changes how an agent follows up.

“Knowing exactly which sections prospects review empowers focused follow-up. If someone spent five minutes on the exclusions page, that is your opening. Address it directly. Agents who do this close faster.” This is the core insight behind digital delivery and engagement visibility as a follow-up strategy.

Engagement features that drive better follow-up:

- Open tracking: know the exact moment a prospect views the proposal

- Section-level tracking: see which coverage areas attract the most attention

- Mobile-optimized viewing: proposals render cleanly on any device, reducing friction

- E-signature integration: clients sign in the same session, eliminating a separate step

- Automated follow-up triggers: if a proposal is unopened after 24 hours, a follow-up SMS fires automatically

Pro Tip: Sort your open pipeline by proposal engagement score each morning. Prospects who viewed the proposal multiple times in the last 24 hours are your hottest leads. Call them first, before your daily schedule fills up with low-priority tasks.

The connection to email marketing for client engagement is direct here. When your proposal tool integrates with your email platform, you can trigger personalized follow-up sequences that reference the specific sections a client engaged with. That level of personalization is simply not possible with a manual process.

Common pitfalls and advanced considerations in proposal automation

Proposal automation has real limits, and agencies that do not plan for them get burned. The most common mistake is treating automation as a set-it-and-forget-it solution. Insurance workflows are document-driven and loaded with exceptions. Automation that works perfectly for standard homeowners policies can fail spectacularly when a commercial client has a unique risk profile.

Automation projects frequently automate the visible front end of the workflow but break downstream when eligibility rules or communications are not fully orchestrated. A quote goes out correctly, but the bind confirmation never fires because the eligibility check ran on an outdated rule set.

Insurance workflows, being document and exception-driven, require explicit validation rules and clearly defined escalation paths for human judgment. Without them, edge cases fall through the cracks and clients experience delays they cannot explain.

Proposal automation quality ultimately depends on two things: data governance and template design. If your intake data is inconsistent, your proposals will be wrong. If your templates are not built around real policy language, your automation will generate documents that require manual correction anyway.

Common failure points to watch for:

- Missing or inconsistent data fields that cause rating engine errors

- Unclear or outdated business rules that misfire on edge case risks

- No escalation path for manual underwriting situations

- Templates that do not account for state-specific disclosure requirements

- Automation that handles quoting but leaves delivery and follow-up entirely manual

- No feedback loop to update rules when real-world errors occur

The automation checklist for insurance agents is a practical starting point for identifying which of these gaps exist in your current setup before you invest in expanding automation.

Pro Tip: Pilot your automation on one product line or one geographic territory first. Run it for 60 days, document every exception and manual override, then use that data to refine your rules before rolling out to the full book.

What most insurance agencies miss about proposal automation

Here is an uncomfortable truth we have seen play out repeatedly: most agencies automate the quote step and declare victory. The showy part, the one that impresses prospects in demos, is the fast quote. But the downstream chaos remains entirely manual.

Agents still copy-paste proposal data into a different system to issue the policy. Follow-up is still tracked on sticky notes or memory. E-signatures are still requested through a completely separate platform. The automation saved 20 minutes on the quote and added 40 minutes of downstream manual work that no one counted.

The real value of proposal automation is only realized when the entire workflow is orchestrated, from the moment a lead enters the system to the moment coverage is bound and the client receives a confirmation. Everything in between needs to talk to everything else.

“The agencies that win with automation are not the ones with the fastest quote engine. They are the ones who built a workflow where nothing falls through the cracks between systems.”

This is why evaluating automation tools requires you to ask one question above all others: what happens after the proposal is sent? If the answer involves manual steps, disconnected platforms, or human memory, you have not automated your proposal process. You have automated one step inside it.

Agencies serious about building scalable, exception-proof workflows should look at AI tools for insurance lead growth as part of a broader automation strategy, not as standalone point solutions. Proposal automation that feeds into AI-powered follow-up and lead scoring creates a compounding advantage over time.

The best practice is simple in concept and hard in execution: start tightly scoped, validate against real-world exceptions, then expand. Agencies that try to automate everything at once typically build a system that handles ideal scenarios perfectly and breaks on anything unusual.

Next steps: automate your proposals and sales processes

Knowing the framework is the first step. Putting it into practice requires the right platform built for how insurance agencies actually work.

CallBack CRM brings together proposal automation, template management, digital delivery, and engagement analytics in one platform designed specifically for insurance agents, agencies, and IMOs. You do not need to stitch together three separate tools to get intake, rating, and delivery connected. The all-in-one automation features cover the full workflow, including CRM management, AI-powered follow-up, and reputation management. For agencies building out their digital presence, the automated website and funnel builder makes it straightforward to capture leads directly into your proposal pipeline. And when a proposal goes out, SMS marketing automation ensures your follow-up fires at exactly the right moment, without you having to remember to send it.

Frequently asked questions

What key stages are involved in insurance proposal automation?

Proposal automation includes intake, rating/pricing, document generation, and digital delivery stages, all managed by configurable workflows that connect each phase automatically.

How does proposal automation improve client follow-up?

Automation tools track client engagement with proposals, showing agents exactly what was viewed and when, so follow-up conversations are targeted and timely rather than generic.

What are the most common failures in proposal automation?

The biggest risk is automating only the front end while leaving eligibility rules and downstream tasks unorchestrated, which causes errors and delays that clients experience as poor service.

Is proposal automation only about generating documents faster?

No. Effective proposal automation transforms the whole workflow from intake to signed delivery, not just the document step. Agencies that treat it as a document shortcut miss most of the operational and client engagement value.