TL;DR:

- Insurance agencies improve profits by focusing on client retention, which is more cost-effective than acquisition. Consistent relationship management and personalized engagement strategies boost loyalty, referrals, and revenue stability. CRM tools and automation help track metrics and maintain ongoing client connections for sustained growth.

Client retention is defined as the ability of an insurance business to keep existing clients active and renewing over time. The importance of client retention goes far beyond avoiding churn. Acquiring a new client costs 5 to 7 times more than keeping one, and improving retention by just 5% can increase profits by 25% to 95%. Those numbers reframe every dollar your agency spends on outreach. Callbackcrm was built specifically for insurance professionals who understand this math and want automation tools that act on it.

What are the key financial benefits of client retention in insurance?

Retention is the most direct lever insurance agencies have for improving profit margins without increasing headcount. The cost savings are immediate. Every client who renews eliminates a full acquisition cycle, including advertising spend, agent time, and onboarding friction.

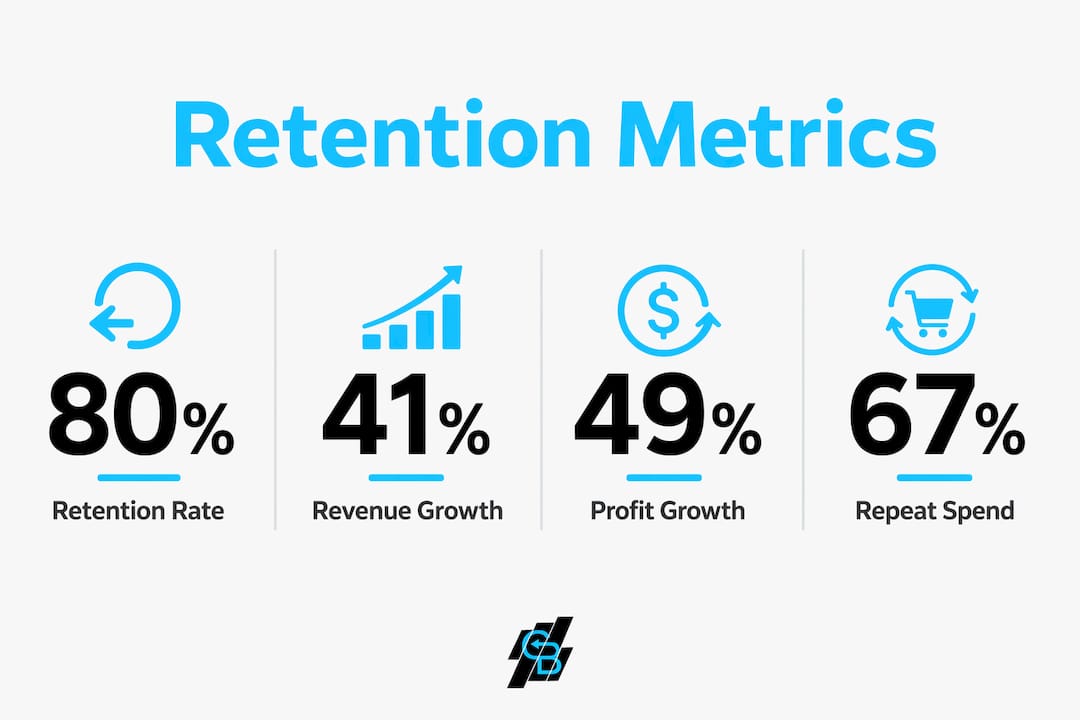

Repeat clients spend 67% more by their third year with a business and require less servicing than new clients. In insurance, that translates to lower claims-handling complexity, faster renewals, and higher cross-sell acceptance rates on products like umbrella policies or life coverage.

Retention-focused companies achieve 41% faster revenue growth and 49% faster profit growth than those prioritizing acquisition. That gap compounds year over year, meaning the agency that invests in keeping clients today will outgrow the agency chasing new leads by a widening margin.

The benefits of customer retention also include referrals. Long-term clients refer friends and family at higher rates than new clients. Referrals arrive pre-sold on your agency’s credibility, which shortens the sales cycle and reduces acquisition cost further.

Key financial advantages of strong retention include:

- Lower cost per client: No repeated advertising or prospecting spend on existing accounts.

- Higher average revenue per client: Cross-sell and upsell rates increase as trust builds.

- Stable cash flow: Renewal-based revenue is predictable, which supports agency planning.

- Referral pipeline: Loyal clients generate new business without additional marketing spend.

- Reduced service cost: Familiar clients need less hand-holding and generate fewer support requests.

How do client loyalty strategies improve retention for insurance businesses?

Loyalty programs in insurance work best when they go beyond price discounts. Effective programs increase client lifetime value and reduce churn by giving clients reasons to stay that have nothing to do with finding a cheaper quote elsewhere. Deloitte’s research confirms that loyalty is increasingly about perceived fairness and value, not rewards points.

For insurance agencies, value-based loyalty tactics produce the most durable results. Consider these four program types:

-

Personalized annual coverage reviews. Schedule a dedicated call or meeting each year to assess whether a client’s coverage still fits their life. A client who just bought a home or had a child needs different coverage. Catching that need first builds trust and prevents them from shopping around.

-

Exclusive risk-management education. Offer webinars, guides, or one-on-one sessions on topics like home safety, business liability, or retirement planning. Clients who learn from you see you as an advisor, not just a vendor.

-

Expedited claims support. Designate a direct contact or priority queue for long-term clients during claims. Speed and clarity during a stressful claim moment creates loyalty that no discount can replicate.

-

Transparent renewal communication. Send renewal notices early, explain any rate changes clearly, and give clients time to ask questions. Frictionless renewal experiences increase retention by respecting how clients actually make decisions.

Authentic loyalty requires frictionless service. Agencies that rely solely on discounts erode their pricing power and train clients to expect lower rates every cycle. That is a race to the bottom that no agency wins.

Pro Tip: Run a quarterly audit of your top 20% of clients by premium value. Assign each one a personal touchpoint, whether a call, a review, or a handwritten note. High-value clients who feel seen renew at significantly higher rates.

What practical tactics help insurance managers improve client retention?

Retention does not happen by accident. It requires deliberate systems, consistent communication, and the right allocation of your team’s time and energy.

Successful agencies allocate 60% of client-facing effort to retention and 40% to acquisition. This 60/40 rule prevents the “leaky bucket” problem, where an agency adds new clients at the top while losing existing ones out the bottom. Without this balance, growth stalls no matter how strong your sales team performs.

CRM use and consistent follow-up are the two most reliable drivers of improved retention. A CRM gives you visibility into which clients are approaching renewal, which have not been contacted recently, and which show early signs of disengagement. That data turns reactive service into proactive relationship management.

Practical retention tactics for insurance managers:

- Segment clients by risk of churn. Use CRM data to flag clients who have not engaged in 90+ days or whose renewal is within 60 days. Prioritize outreach to this group first.

- Automate follow-up sequences. Set up SMS or email workflows that trigger at key moments: 90 days before renewal, after a claim closes, and on a client’s policy anniversary.

- Use cross-sell data to add value. Clients with only one policy are more likely to leave. Identify single-policy holders and offer a coverage gap analysis.

- Avoid discount-based retention. Value-driven rewards like personalized reviews and risk-management resources build commitment that price cuts cannot.

- Track satisfaction signals. A simple Net Promoter Score survey after each renewal or claim gives you early warning before a client decides to leave.

Pro Tip: Use personalized marketing outreach to send clients content relevant to their specific policy type. A homeowner client who receives a home safety checklist before hurricane season feels served, not sold to.

What metrics should insurance firms track to measure client retention?

Measuring client retention requires tracking five core metrics. Without them, you are managing relationships by instinct rather than evidence.

| Metric | What it measures | Target benchmark |

|---|---|---|

| Retention rate | Percentage of clients who renew each period | Above 80% is good; above 90% is excellent |

| Churn rate | Percentage of clients lost in a given period | Below 10% annually is a healthy target |

| Client lifetime value | Total revenue a client generates over the relationship | Track trend year over year |

| Average relationship length | Mean duration of client relationships in years | Rising trend signals healthy retention |

| Net Promoter Score | Client willingness to refer your agency | Above 50 indicates strong loyalty |

These five metrics work together to give a complete picture of retention health. Retention rate tells you the outcome. Churn rate tells you the rate of loss. Client lifetime value tells you the financial weight of each relationship. Average relationship length tells you whether your book of business is aging well. Net Promoter Score tells you whether clients would put their reputation behind yours.

Cohort analysis adds another layer of insight. Group clients by the year they joined and track how each cohort’s retention rate changes over time. If clients who joined in 2022 retain at 88% but clients from 2024 retain at 74%, that gap signals a problem with your onboarding or early-relationship experience. CRM data makes this analysis straightforward when fields are consistently filled.

AI-driven CRM tools can automate much of this tracking, flagging at-risk clients before they reach the decision to leave. Reviewing these metrics monthly, not just at year-end, gives your team time to act on the data. For more on proven retention strategies that apply across service industries, external research reinforces many of the same principles.

Kyle’s take: retention is a discipline, not a campaign

Most insurance agencies treat retention as something they do when renewal season arrives. That is the wrong frame entirely. Retention is a continuous discipline that runs in the background of every client interaction, every claim, and every policy change conversation.

The agencies I have seen grow steadily over a decade share one habit: they treat every renewal moment as a relationship checkpoint, not a transaction. They ask whether the client’s coverage still fits. They explain rate changes before the client calls to complain. They make the renewal feel like a service, not a bill.

Short-term discounts are the most common mistake I see. An agency drops the premium to keep a client, and that client stays for another year. But now they expect a discount every cycle, and the relationship is built on price rather than trust. When a competitor offers a lower rate, that client leaves anyway. Relationship marketing built on genuine value is the only version that compounds.

The other mistake is treating retention as a separate initiative from service quality. They are the same thing. A client who gets a fast, clear answer during a claim does not shop around at renewal. A client who waits three days for a callback does. Every service interaction is a retention event. Build your team’s habits around that reality, and the metrics will follow.

— Kyle

How Callbackcrm supports insurance client retention

Insurance agencies that want to act on retention data need tools that connect communication, CRM records, and automation in one place.

Callbackcrm’s SMS marketing features let insurance teams send personalized renewal reminders, policy anniversary messages, and post-claim check-ins automatically, triggered by CRM data. That means no client falls through the cracks because a renewal date was missed or a follow-up was forgotten. The platform’s AI-driven workflows identify which clients need attention and when, so your team focuses on conversations rather than calendar management. For agencies ready to build a retention system that runs consistently, Callbackcrm provides the infrastructure to make it work at scale.

FAQ

Why does client retention matter more than acquisition?

Retaining a client costs 5 to 7 times less than acquiring a new one, and a 5% improvement in retention can increase profits by 25% to 95%. Acquisition fills the bucket; retention keeps it from leaking.

What is a good client retention rate for insurance agencies?

A retention rate above 80% is considered good for insurance agencies, and above 90% is excellent. Tracking this metric monthly gives teams time to intervene before churn accelerates.

How do loyalty programs help insurance businesses retain clients?

Loyalty programs that offer personalized coverage reviews, risk-management education, and expedited claims support build trust that price discounts cannot replicate. Deloitte research confirms that perceived fairness and value drive loyalty more than rewards points alone.

What is the 60/40 rule in insurance client retention?

The 60/40 rule means allocating 60% of client-facing effort to retention activities and 40% to new client acquisition. This balance prevents revenue loss from churn while still supporting agency growth.

How does CRM data improve client retention in insurance?

CRM data identifies clients approaching renewal, those who have not been contacted recently, and early churn signals. Consistent follow-up driven by CRM insights is one of the strongest predictors of improved retention rates.

Key takeaways

Client retention is the single highest-return investment an insurance agency can make, because it reduces costs, increases revenue per client, and generates referrals simultaneously.

| Point | Details |

|---|---|

| Retention beats acquisition on cost | Keeping a client costs 5 to 7 times less than acquiring a new one. |

| Value-based loyalty outperforms discounts | Personalized reviews and risk-management resources build commitment that price cuts cannot. |

| The 60/40 rule prevents revenue leakage | Allocate 60% of client-facing effort to retention and 40% to acquisition. |

| Five metrics reveal retention health | Track retention rate, churn rate, client lifetime value, relationship length, and Net Promoter Score monthly. |

| Automation closes the follow-up gap | CRM-driven workflows ensure no renewal or post-claim touchpoint is missed. |