TL;DR:

- Predictive lead scoring uses machine learning to analyze historical data and rank prospects by their likelihood of converting. It significantly improves insurance sales outcomes by targeting high-intent leads faster and aligns sales and marketing efforts effectively. Implementing a simple, transparent model with quality data can deliver measurable ROI within weeks.

Most insurance sales teams treat every lead the same way. They call down the list, chase whoever picks up, and wonder why conversion rates stay flat. Predictive lead scoring fixes that problem at the source. If you have wondered what is predictive lead scoring and whether it actually applies to your agency or IMO, the short answer is: yes, absolutely, and it is less complicated than you think. This guide breaks down the lead scoring definition, how the models work with insurance-specific data, and exactly what you can expect when you implement one.

Table of Contents

- Key takeaways

- What predictive lead scoring actually is

- The data that makes insurance scoring models work

- How predictive scoring improves insurance sales outcomes

- How to implement predictive lead scoring step by step

- Comparing predictive scoring to other scoring methods

- My honest take on predictive lead scoring in insurance

- See predictive lead scoring in action with Callbackcrm

- FAQ

Key takeaways

| Point | Details |

|---|---|

| Not just a ranking system | Predictive lead scoring uses machine learning to find patterns in historical data, not arbitrary point assignments. |

| Insurance signals are different | Renewal timing, incumbent carrier, and coverage type are the most predictive variables for insurance leads. |

| Data quality determines accuracy | Dirty or insufficient training data is the most common reason scoring models fail before they ever launch. |

| Simple models often win | A five-factor model that sales reps understand beats a black-box algorithm they do not trust. |

| ROI is measurable | Agencies report up to 30% better campaign ROI when they shift from manual sorting to predictive scoring. |

What predictive lead scoring actually is

At its core, the lead scoring definition is simple: it is a method for ranking prospects by their likelihood to convert. Traditional point-based scoring does this by assigning fixed values to actions. Someone downloads a whitepaper? Give them 10 points. They open three emails? Add 15 more. It feels systematic, but it is mostly guesswork dressed up as data.

Predictive lead scoring is fundamentally different. Instead of hand-crafting rules, you feed a machine learning model your historical conversion data. The model identifies which combinations of signals actually predicted past conversions and uses those patterns to score new leads automatically. The scores continuously update as more sales outcomes feed back into the system.

Here is what makes predictive scoring models distinctly powerful. They can detect non-linear, complex patterns that a human rule-builder would never think to encode. For example, a prospect who requests a commercial auto quote after visiting your claims process page twice within a week might score dramatically higher than someone who downloaded the same whitepaper. A point-based system would miss that interaction entirely.

For insurance, this matters because the buying signals are highly specific:

- A policy up for renewal in the next 90 days is a fundamentally different prospect than one that renewed last month.

- A business owner with a gap in general liability coverage signals urgency a generic model would never capture.

- Behavioral signals like quote requests, calculator use, and FAQ page visits carry far more weight than simple email opens.

Predictive scoring accuracy can reach 85 to 90% with sufficient historical data. That is not perfect, but it is far better than gut feeling or static point assignments.

Pro Tip: Start tracking conversion outcomes in your CRM immediately, even before you build a model. Every closed deal and lost opportunity you record today becomes training data that makes your future model more accurate.

The data that makes insurance scoring models work

Predictive scoring models are only as good as the features you put into them. In insurance, the data inputs split into two distinct categories: fit and intent.

Fit data tells you whether a prospect matches your ideal customer profile regardless of their current behavior. In insurance, that includes business size, industry class code, geographic location, years in business, and current coverage structure.

Intent data tells you whether a prospect is actively considering a purchase. This is where insurance scoring diverges most sharply from generic B2B models. Renewal timing is the single most predictive variable for near-term purchase intent, yet it gets ignored in most off-the-shelf scoring tools.

The strongest insurance-specific scoring variables include:

- Policy renewal date (within 30, 60, or 90 days)

- Incumbent carrier relationship and any known dissatisfaction signals

- Lines of coverage currently held versus lines they have requested quotes for

- Prior claim history or recent life events like a business acquisition

- Website behavior: quote requests, coverage calculator completions, and FAQ engagement

- Email engagement patterns tied to specific coverage topics

| Data type | Example variable | Why it matters for insurance |

|---|---|---|

| Renewal timing | Days until policy expiration | Strongest near-term purchase intent signal |

| Incumbent carrier | Current insurer name | Reveals switching likelihood and competitive positioning |

| Coverage gap | Missing liability or umbrella | Creates urgency and cross-sell opportunity |

| Behavioral signal | Quote request submitted | High-intent action with direct conversion correlation |

| Life event | Business acquisition or expansion | Triggers new coverage needs immediately |

Data quality is not optional. Dirty or insufficient training data is the leading cause of model failure, not algorithmic complexity. Before you build anything, audit your CRM for duplicate records, inconsistent fields, and missing renewal dates.

Pro Tip: If your CRM is missing renewal dates for more than 30% of your book, fix that first. A data enrichment sprint before model development will pay for itself many times over in scoring accuracy.

How predictive scoring improves insurance sales outcomes

The business case for predictive lead scoring in insurance is not theoretical. Agencies implementing these models have reported a 30% improvement in campaign ROI and a measurable increase in sales productivity compared to manual prioritization.

The mechanism is straightforward. When your agents spend their first two hours every morning calling the top-scored leads instead of working through a flat list, more of those conversations happen at the right moment. A prospect who scores 87 out of 100 because their policy renews in 45 days and they visited your commercial auto page three times last week will answer a well-timed call very differently than a cold prospect.

“The biggest ROI from lead scoring is not conversion rate alone. It is the sales time recaptured from low-probability prospects and redirected toward high-intent ones. That time has real dollar value.”

Predictive scoring also solves one of the most persistent problems in insurance agencies: sales and marketing misalignment. Marketing runs a campaign, passes leads to sales, and sales complains the leads are not qualified. With a shared scoring model, both teams are working from the same definition of what a qualified lead looks like. Marketing can optimize campaigns toward leads that score above a set threshold. Sales can trust that a high-scoring lead is worth their immediate attention. You can learn more about aligning sales and marketing with predictive generation strategies on the Callbackcrm blog.

The practical effects compound over time. As the model learns from more conversion outcomes, scores get sharper. Routing rules become more precise. High-scoring leads get called within an hour. Mid-tier leads go into nurture sequences. Low-scoring leads get automated touches until their situation changes.

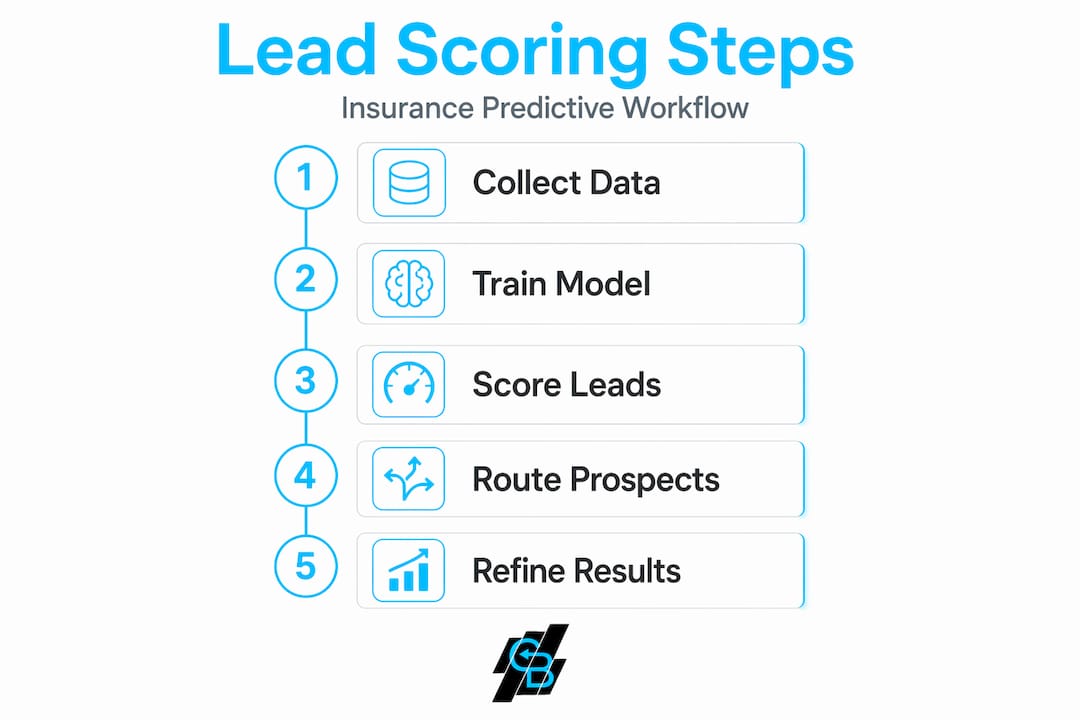

How to implement predictive lead scoring step by step

Getting a predictive scoring model live in an insurance context does not require a data science team. Here is a realistic roadmap:

-

Audit your historical data. You need at minimum 40 converted and 40 lost leads to train an initial model, though 1,000 or more examples are recommended for reliable performance. A two-year lookback window is standard for insurance given seasonal renewal patterns. Practically speaking, models trained on fewer than 1,000 positive examples often fail to detect meaningful conversion patterns.

-

Involve your sales team from day one. Ask your top producers which signals they use to mentally qualify a lead. Their instincts contain real pattern knowledge that improves model design. Sales team input throughout model design is one of the most reliable predictors of adoption success.

-

Start with a simple model. A five-factor model built around age, income, current coverage, recent life events, and response history often outperforms more elaborate versions. Simple models are easier to explain, easier to trust, and easier to maintain.

-

Integrate with your CRM and marketing automation. Scores need to be visible where agents work. If a rep has to log into a separate tool to check a lead score, they will not do it consistently. The score should appear on the lead record automatically and trigger routing rules without manual input.

-

Set clear follow-up protocols by score band. A score above 80 should trigger a same-day call. A score between 50 and 79 goes into a structured nurture sequence. Clear processes for acting on scores are what separate teams that realize ROI from teams that just have a cool model sitting in the background.

-

Run a 30-day test and refine. Compare conversion rates for high-scored leads versus your baseline. Adjust feature weights based on what the outcomes show. Most initial models go live within four to eight weeks and then enter a continuous improvement cycle.

Pro Tip: Build a simple lead scoring process guide specific to your agency so every agent knows what a score of 80+ means and what they are expected to do with it. Technology without process does not convert.

Comparing predictive scoring to other scoring methods

Not every scoring approach serves the same purpose. Understanding the types of lead scoring helps you pick the right tool for each stage of your pipeline.

| Scoring type | What it evaluates | Best use case in insurance |

|---|---|---|

| Traditional point-based | Fixed rule scores tied to specific actions | Small agencies with limited data history |

| Predictive lead scoring | ML-driven probability based on historical conversions | Mid-to-large agencies with sufficient CRM history |

| Opportunity scoring | Likelihood of closing an active deal | Commercial lines with long, complex sales cycles |

Opportunity scoring is distinct from predictive lead scoring because it evaluates existing deals in your pipeline rather than new or potential leads. Both are useful, but they answer different questions. Predictive lead scoring asks: “Which prospects should we pursue first?” Opportunity scoring asks: “Which deals are we most likely to close this quarter?”

For most insurance agencies, predictive lead scoring delivers the most immediate impact because it addresses the top-of-funnel problem: too many leads, not enough clarity on where to focus. You can also explore lead nurturing strategies to understand how scoring integrates with broader funnel management.

My honest take on predictive lead scoring in insurance

I have seen agencies spend months building sophisticated scoring models that their sales team never trusted enough to use. The model sat in the CRM like expensive furniture nobody sat on.

What I have learned is that the technology is rarely the problem. The adoption challenge is almost always about transparency and involvement. When sales reps understand why a lead scores the way it does, they act on it. When the score feels like a black box, they revert to their own instincts and the model becomes irrelevant.

My strongest recommendation: build the simplest model that your best agent would recognize as logical. If your top commercial lines producer looks at the scoring criteria and says “yes, that is how I think about it too,” you have something that will actually get used. Complexity can always come later. Trust cannot be retrofitted.

The other thing I would caution against is writing off low-scoring leads entirely. A prospect who scores 35 today because they just renewed might score 90 in nine months. The real value of predictive scoring is not just who you call today. It is building a nurture system that catches the right leads at exactly the right moment in their renewal cycle. That timing advantage is where insurance-specific scoring genuinely separates itself from generic tools.

— Kyle

See predictive lead scoring in action with Callbackcrm

Callbackcrm is built specifically for insurance agencies and IMOs that want to move beyond spreadsheets and gut instinct. The platform includes AI-powered lead scoring built into your CRM, so scores appear automatically on every lead record without a separate tool or manual data entry.

Beyond scoring, Callbackcrm connects your lead prioritization directly to your marketing automation features, SMS outreach, and funnel tools so your highest-scoring leads get the right message at the right moment. When a prospect’s renewal date triggers a score spike, an automated follow-up sequence can launch before a human even touches the record. Explore the full feature set to see how AI scoring, SMS marketing, and website capture tools work together to turn your lead data into closed policies.

FAQ

What is predictive lead scoring in simple terms?

Predictive lead scoring uses machine learning to analyze historical sales data and assign each prospect a probability score reflecting their likelihood to convert. Unlike traditional scoring, the model learns from actual outcomes rather than manually assigned point values.

How much data do I need to start?

You need at minimum 40 converted and 40 lost leads to train an initial model, but 1,000 or more examples produce significantly more reliable results. A two-year lookback window is standard for insurance agencies.

What makes insurance lead scoring different from B2B scoring?

Insurance scoring requires variables specific to the industry, particularly renewal timing, incumbent carrier relationships, and lines of coverage. Generic B2B models typically omit these signals, reducing accuracy for insurance prospects significantly.

How long does it take to implement a predictive scoring model?

Most teams can ship an initial model in four to eight weeks, followed by a continuous optimization period as the system learns from new conversion outcomes over time.

Will predictive scoring replace my sales team’s judgment?

No. The model surfaces which leads deserve immediate attention; your sales team still handles the relationship and the close. The best implementations treat scoring as a prioritization tool that amplifies good sales instincts, not one that replaces them.